Daily Market Update 08.10 | Stocks Surge After CPI Data Release!

MyntBit's Daily Market Update is dedicated to providing traders with a recap and bringing setups to watch for the next trading day.

Today's Recap

Market Snapshot

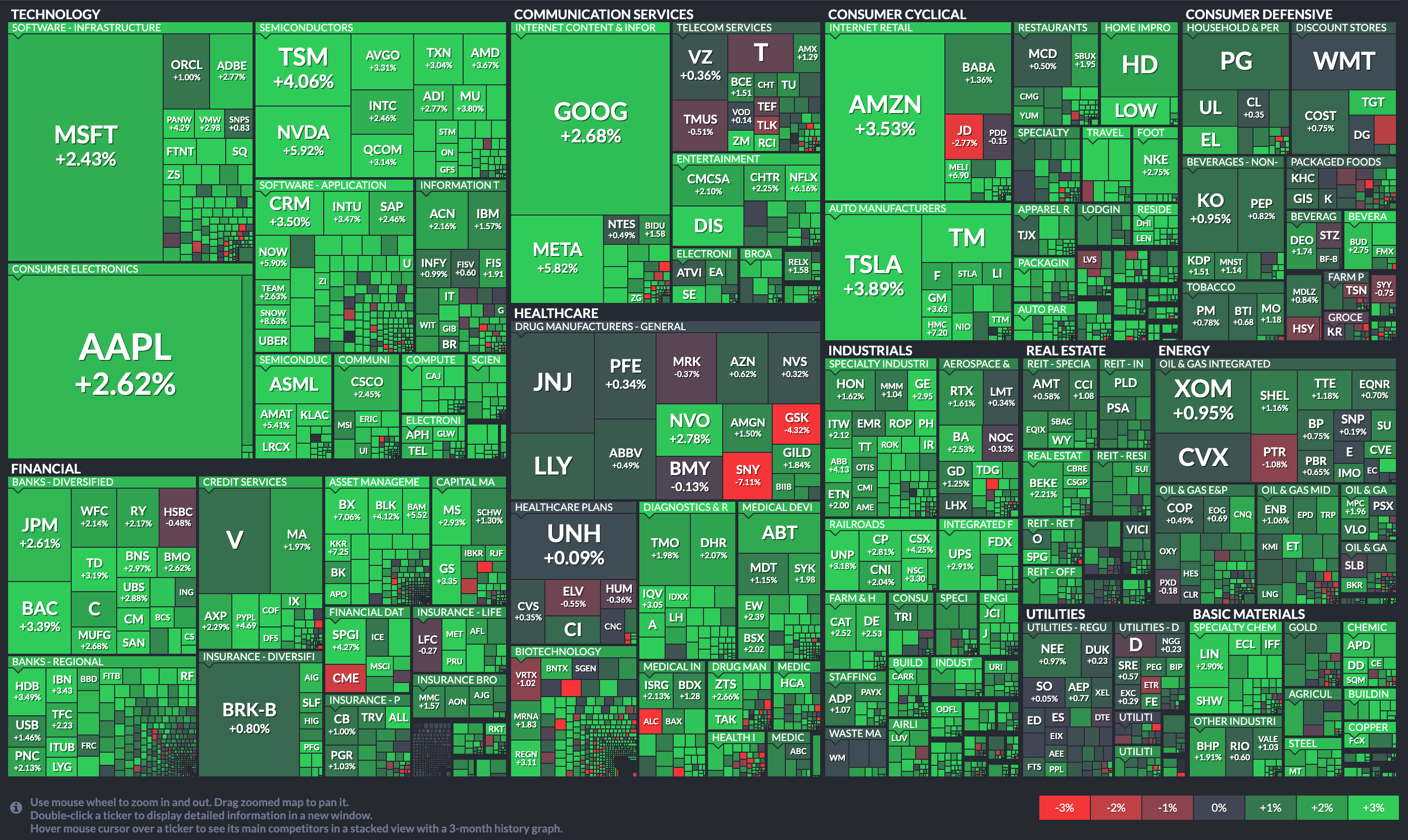

Market Heatmap

RTTNews Market Update

With traders reacting positively to highly anticipated consumer price inflation data, stocks moved sharply higher during trading on Wednesday. The rally more than offset the weakness seen in the previous session, with the major averages reaching three-month closing highs.

The major averages all finished the day firmly in positive territory. The Dow jumped 535.10 points or 1.6 percent to 33,309.51, the Nasdaq spiked 360.88 points or 2.9 percent to 12,854.80 and the S&P 500 surged 87.77 points or 2.1 percent to 4,210.24.

The rally on Wall Street came after the Labor Department released a report showing U.S. consumer prices unexpectedly came in flat in the month of July.

The Labor Department said its consumer price index was unchanged in July after jumping by 1.3 percent in June. Economists had expected consumer prices to edge up by 0.2 percent.

Compared to the same month a year ago, consumer prices in July were up by 8.5 percent, reflecting a bigger than expected slowdown from the 9.1 percent spike in June.

The annual rate of price growth was expected to slow to 8.7 percent from the four-decade high seen in the previous month.

Meanwhile, the report said core consumer prices, which exclude food and energy prices, rose by 0.3 percent in July after climbing by 0.7 percent in June. Core prices were expected to increase by 0.5 percent.

The annual rate of core consumer price growth was unchanged at 5.9 percent, while economists had expected an acceleration to 6.1 percent.

The tamer than expected inflation data has led to speculation that the Federal Reserve will slow the pace of interest rate hikes at its September meeting.

CME Group's FedWatch tool is currently indicating a 56.5 percent chance of a 50 basis point rate hike and a 43.5 percent chance of a 75 basis point rate hike.

"Today's inflation report might lead the Fed to downshift the size of its rate hikes to 50bps in September," said Kathy Bostjancic, Chief U.S. Financial Economist at Oxford Economics.

She added, "However, we still see 75bps as likely given the ongoing inflation pressures, still elevated inflation readings, and ongoing tight labor market that is leading to large wage gains."

Sector News

Semiconductor stocks showed a substantial rebound after pulling back sharply in recent sessions, resulting in a 4.3 percent spike by the Philadelphia Semiconductor Index.

Considerable strength was also visible among computer hardware stocks, as reflected by the 4 percent surge by the NYSE Arca Computer Hardware Index. The index ended the session at its best closing level in two months.

Networking stocks also turned in a strong performance on the day, driving the NYSE Arca Networking Index up by 3.6 percent to a three-month closing high.

Housing, transportation and banking stocks also saw considerable strength, moving higher along with most of the other major sectors.

Other Markets

In overseas trading, stock markets across the Asia-Pacific region moved mostly lower during trading on Wednesday. Japan's Nikkei 225 Index slid by 0.7 percent, while Hong Kong's Hang Seng Index plunged by 2 percent.

Meanwhile, the major European markets moved to the upside on the day. While the German DAX Index jumped by 1.2percent, the French CAC 40 Index climbed by 0.5 percent and the U.K.'s FTSE 100 Index rose by 0.3 percent.

In the bond market, treasuries gave background after an early rally but still closed modestly higher. As a result, the yield on the benchmark ten-year note, which moves opposite of its price, edged down by 1.1 basis points to 2.786 percent after hitting a low of 2.674 percent.

Looking Ahead

Trading on Thursday may be impacted by reaction to a pair of Labor Department reports on weekly jobless claims and producer price inflation.

On the earnings front, entertainment giant Disney (DIS) is among the companies releasing their quarterly results after the close of today's trading.

$DIS is expected to show a

rise in third-quarter revenue, helped by

steady subscriber growth on its

streaming platforms accompanied by a

resumption in its theme parks.— Sylwia (@i_sylwiaa) August 10, 2022

But, as of now, nothing has changed from our weekly perspective.

CPI Coming Up NEXT Week! Could It CRASH The Market? | Weekly Market Update

Tomorrow's Plan

/ES - Emini S&P 500

On /ES, we opened around the 4178 level, and we experienced choppiness for most of the day. The HOD was 4213. /ES did not break into lower levels as AAPL showed strength today closing at $169.24. There is one more gap to the upside to close on AAPL in the $173-175 area. Also, DXY and VIX went down. If DXY continues falling, tech stock might see a further rally, which in turn will make /ES reach 4245, possibly 4300.

Bullish Scenario

If we OPEN above again 4207 (POC), we will need to go above 4213, then 4222, 4240, 4280, and 4300.

Bearish Scenario

If we OPEN below 4207, we can see 4193, 4180, 4160, 4140, 4120

POC: 4207 | Range: 3723 - 4300

/NQ - Emini Nasdaq 100

On the /NQ side, POC today was 13356, VH 13397, VL 13293

Bullish Scenario

If we OPEN above 13356, to see further upside, we need to overcome VH 13397, then 13450, 13500, and 13789 (which might serve as a strong resistance).

Bearish Scenario

If we OPEN below 13356, we will need to retest VL 13293, 13234, 13200, 13160, and 13000.

POC: 13356 | Range: 11390 - 13583

For the stock watchlist from the weekend and daily updates, please watch the below videos…

Earnings Calendar

Economic Calendar

Disclaimer: This newsletter is not trading or investment advice, but for general informational purposes only. This newsletter represents our personal opinions which we are sharing publicly for educational purposes. Futures, stocks, bonds trading of any kind involves a lot of risk. No guarantee of any profit whatsoever is made. In fact, you may lose everything you have. So be very careful. We guarantee no profit whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this newsletter, its representatives, its principals, its moderators and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission, CFTC or with any other securities/regulatory authority. Consult with a registered investment advisor, broker-dealer, and/or financial advisor. Reading and using this newsletter or any of my publications, you are agreeing to these terms. Any screenshots used here are the courtesy of IBKR, Unusual whales, RTTnews, FXstreet, and/or Tradingview. We are just an end-user with no affiliations with them.